Airbus vs. Boeing in January 2026: Who Had The Best Start To The Year?

The first month of 2026 has delivered a surprisingly clear contrast between Boeing and Airbus in both orders and deliveries, offering early clues about how each manufacturer’s year may unfold.

While January is traditionally a quieter month—often shaped by the tail end of previous‑year campaigns and the slow ramp‑up after the holiday period—the numbers reveal meaningful differences in momentum, customer confidence, and production stability.

Orders: Boeing Opens 2026 With a Commanding Lead

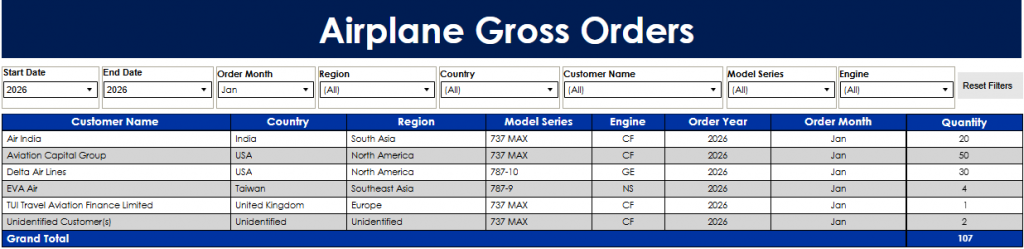

Boeing’s January orderbook is the standout story. With 107 gross orders, the US manufacturer has begun the year with a level of commercial traction that Airbus simply did not match.

The bulk of the American planemaker’s activity came from three major deals:

- Aviation Capital Group – 50 Boeing 737 MAX aircraft

- Delta Air Lines – 30 Boeing 787‑10s

- Air India – 20 Boeing 737 MAX aircraft

These three customers alone account for 100 of the American planemaker’s 107 orders, signalling strong leasing‑sector confidence and continued widebody demand from US carriers.

The Delta order is particularly notable: the 787‑10 has been gaining momentum as airlines seek high‑capacity, long‑haul efficiency without stepping into the ultra‑long‑range segment.

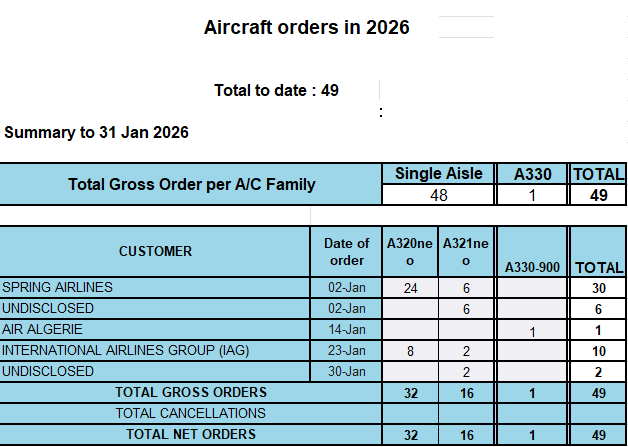

Airbus, by contrast, recorded 49 gross orders, less than half of Boeing’s total. The European manufacturer’s activity was dominated by:

- Spring Airlines – 30 A320neo family aircraft

- IAG – 10 A320neo family aircraft

- Two undisclosed customers – 8 A321neos

- Air Algérie – 1 A330‑900

Airbus’ January orders are respectable, especially given the strength of the A321neo, but the absence of a major headline‑grabbing deal—particularly in the widebody segment—creates a softer start compared to Boeing’s blockbuster month.

Early Indicator: Boeing’s sales momentum is clearly stronger

The MAX continues to attract large leasing‑company commitments, and the 787‑10’s resurgence hints at a potentially strong year for Boeing’s widebody program.

Airbus, meanwhile, remains heavily reliant on the A320neo family, with the A350 and A330neo seeing minimal early‑year activity.

Deliveries: Boeing Leads in Volume, Airbus Shows Stability

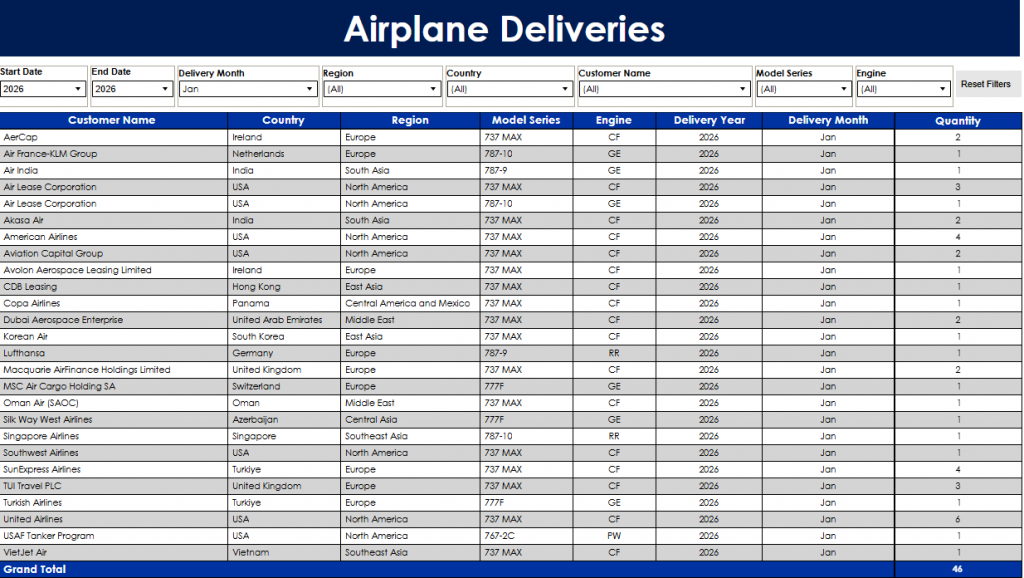

Deliveries tell a slightly different story. The American manufacturer delivered 46 aircraft in January, while Airbus delivered 19.

On volume alone, the American planemaker is ahead—but the composition of those deliveries is where the nuance lies.

Boeing Deliveries – 46 Total

- 737 MAX: 36 deliveries

- 787 family: 4 deliveries

- 777F: 4 deliveries

- 767‑2C (USAF Tanker Program): 1 delivery

The MAX dominated the American planemaker’s output, with deliveries spread across a wide range of customers including United Airlines (6), American Airlines (4), SunExpress (4), and Air Lease Corporation (3).

The freighter segment also remained active, with MSC Air Cargo, Silk Way West Airlines, and Turkish Airlines each receiving 777Fs.

This distribution suggests the U.S manufacturer narrowbody production line is stabilising, though still not at pre‑grounding or pre‑pandemic levels.

The presence of multiple 787‑9 and 787‑10 deliveries also indicates continued recovery in the widebody program.

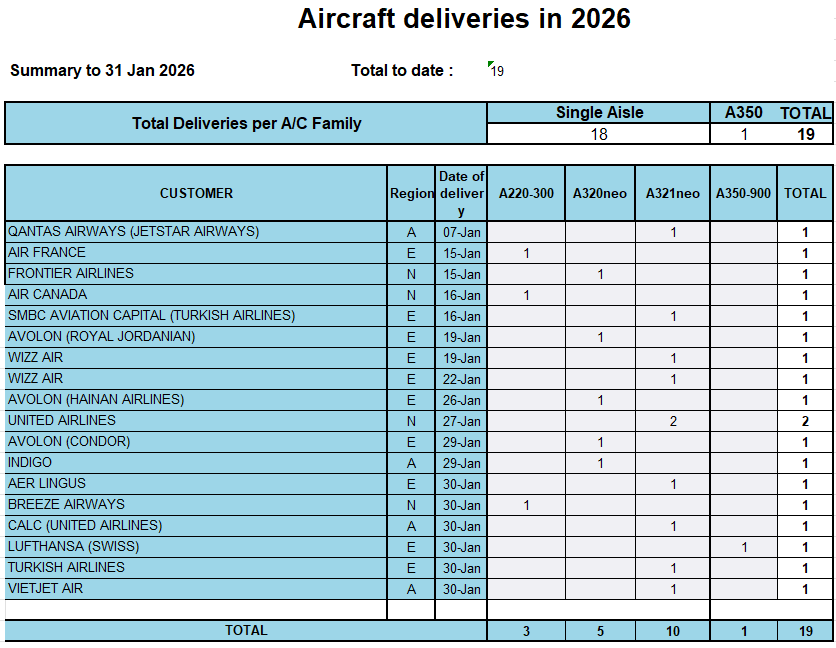

Airbus Deliveries – 19 Total

- A321neo: 10 deliveries

- A320neo: 5 deliveries

- A220‑300: 3 deliveries

- A350‑900: 1 delivery

Airbus’ deliveries are more evenly spread across its single‑aisle families, with the A321neo continuing to dominate.

The A350‑900 delivery to Lufthansa (Swiss) is the only widebody handover of the month.

While Airbus’ total volume is lower, the consistency of its single‑aisle output reflects a production system that is steady, predictable, and less prone to the volatility that has characterised the American planemaker’s recent years.

If Boeing can maintain this pace without quality‑control setbacks, it could widen the delivery gap significantly in 2026.

Airbus, however, may be better positioned to avoid disruptions.

What January Suggests About the Year Ahead

1. Boeing’s sales pipeline is heating up

The scale of Boeing’s January orders—particularly from lessors—signals renewed confidence in the MAX and strong demand for the 787‑10.

If this trend continues, Boeing could reclaim orderbook leadership in 2026 after several turbulent years.

2. Airbus remains the single‑aisle powerhouse

Even with fewer orders and deliveries, Airbus’ A321neo continues to dominate its mix.

The aircraft’s unmatched range‑capacity combination keeps it in high demand, and Airbus’ backlog remains enormous.

January’s numbers don’t reflect weakness, just the absence of a major campaign closing.

3. Widebody demand is shifting

Boeing’s 787‑10 activity and Airbus’ quiet A350 month suggest a potential tilt toward Boeing in the long‑haul segment early in the year.

But widebody orders tend to be lumpy, and Airbus could easily rebalance this with a single large campaign.

4. Deliveries will depend on supply chain resilience

Both manufacturers continue to face engine‑related constraints, particularly on the A320neo family and 737 MAX.

January’s output hints at gradual improvement, but the true test will come in Q2 and Q3.

Boeing Starts 2026 With the Stronger Hand

Based solely on January, the American planemaker has clearly outperformed Airbus in both orders and deliveries.

The US manufacturer enters 2026 with renewed commercial momentum, strong leasing‑sector confidence, and a delivery profile that is beginning to resemble pre‑crisis levels.

Airbus, while quieter, remains stable and strategically well‑positioned—especially in the single‑aisle market.

The year is long, and one month does not define a trend, but the early signals suggest that the American planemaker is determined to make 2026 a year of regained ground.

Continue to follow The Aviation Hub for more analysis and insight!